2024 has been quite a year for gold and silver. And it looks like there is more to come.

Here is a one-year chart of the gold price:

Please note the bullish technical indicators, with the red line indicating the 200-day moving average price and the blue line the shorter term 50-day moving average. Gold is trading above both trend lines.

Here is a one-year silver chart:

As did gold, silver made a strong breakout in March. It has mostly traded above both the short- and long-term trendlines since April, although it broke below the 50-day moving average on Friday, 7/19, on profit taking.

And finally, here is a one-year chart reflecting the ratio of gold and silver prices:

Note that this is not a price chart. It reflects the relative prices of the two precious metals. The gold/silver ratio has been trending down since May. You should speak with your Republic Monetary Exchange representative about this. The ratio indicates that silver is still advantageously priced relative to the gold price and you continue to have an opportunity to trade gold for silver while silver is historically underpriced compared to gold and therefore poised for faster price appreciation. But the gold-silver ratio is on the move and that advantage may not last.

Contact Republic Monetary Exchange today and learn more about this profitable strategy.

Is the United States insolvent? By that I mean is it unable to pay its debts?

The honest answer is yes. The formal answer is no.

Let us explain.

Better yet, let Ben Bernanke, the former Chairman of the Federal Reserve System explain:

“The US government has a technology, called a printing press, that allows it to produce as many dollars as it wishes at essentially no cost.”

Dr. Bernanke was one of the great money printers of all time. In other words, he was one of the great inflationists of all time:

“Under a paper-money system, a determined government can always generate higher spending and, hence, positive inflation.”

So, no matter how much debt the government has, it can print money to pay its creditors. This legalized counterfeiting is a fraud. You can’t pay off your creditors by doing the same thing without going to jail. But the government can. Unfortunately, there is no such thing as a free lunch and there is a reason people go to jail for counterfeiting. That is because it defrauds others. Even when the government does it and calls it legal.

The new money the government prints takes on value or purchasing power to the extent that the existing money (your savings) loses value or purchasing power. That loss of purchasing power is commonly called inflation.

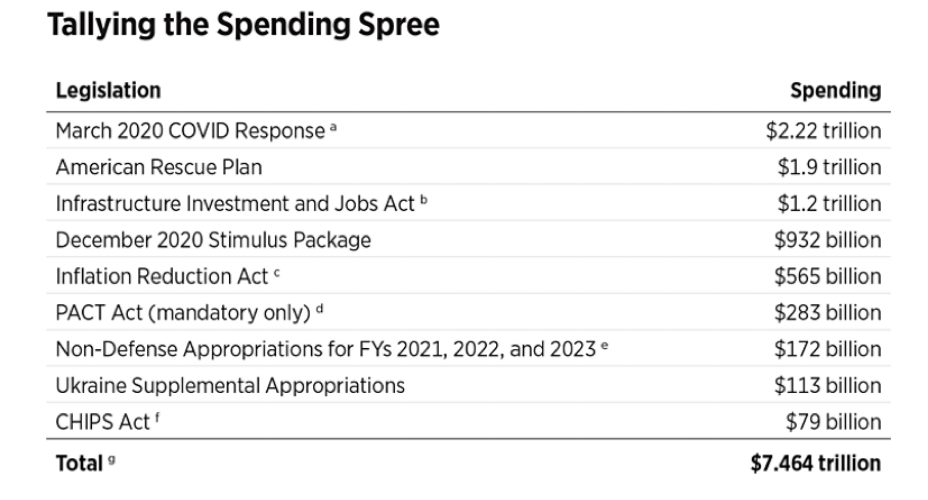

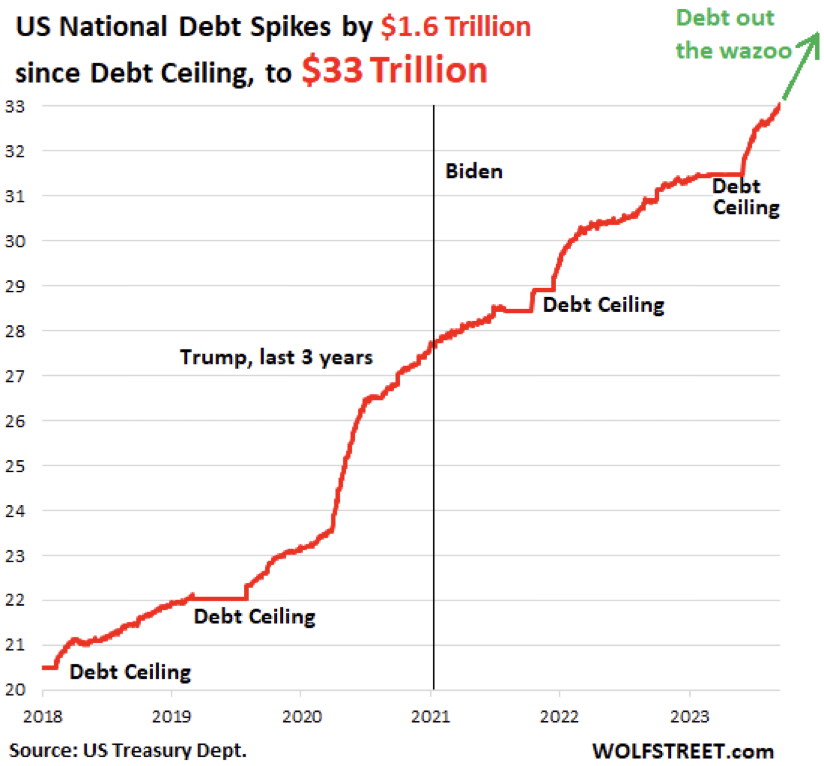

The USGoverment ran a $1.3 trillion deficit for the first nine months of this fiscal year. It is about $1.85 trillion as we write this.

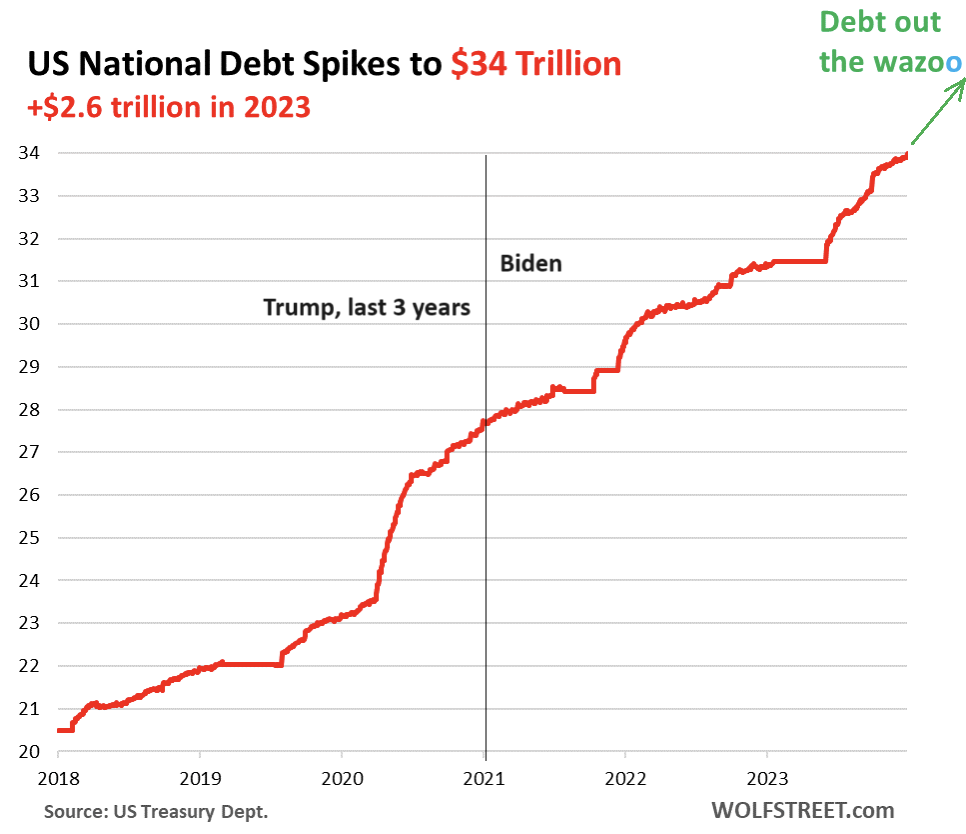

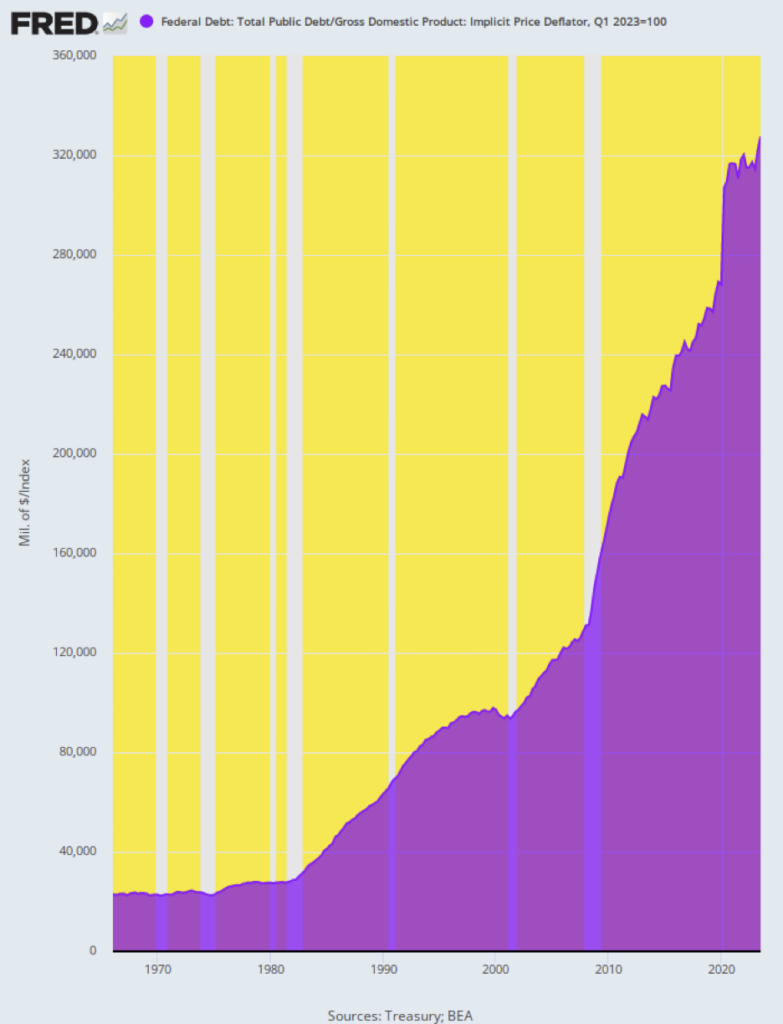

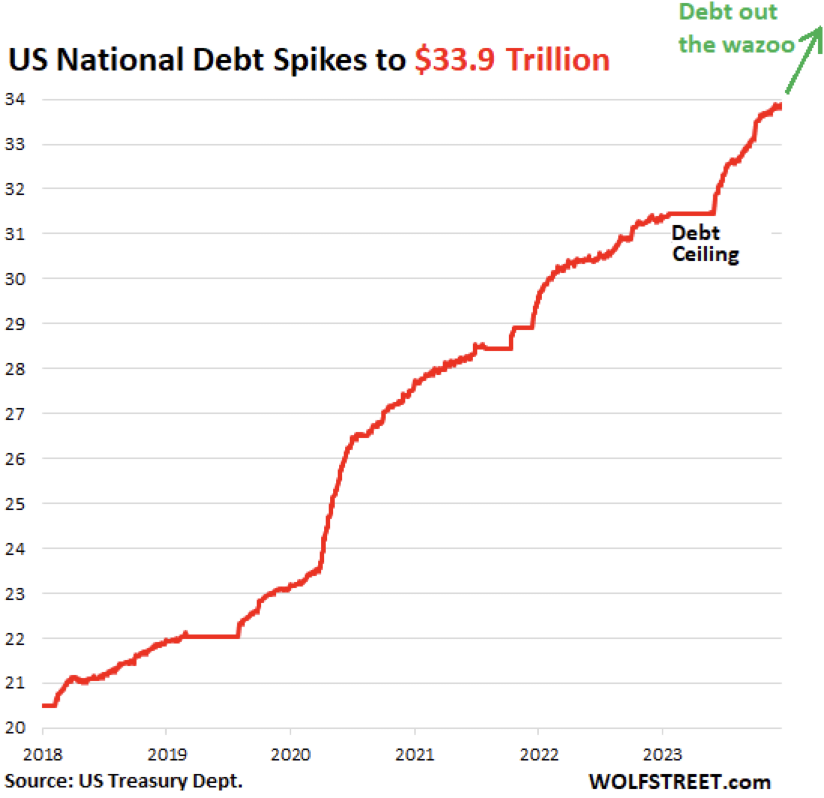

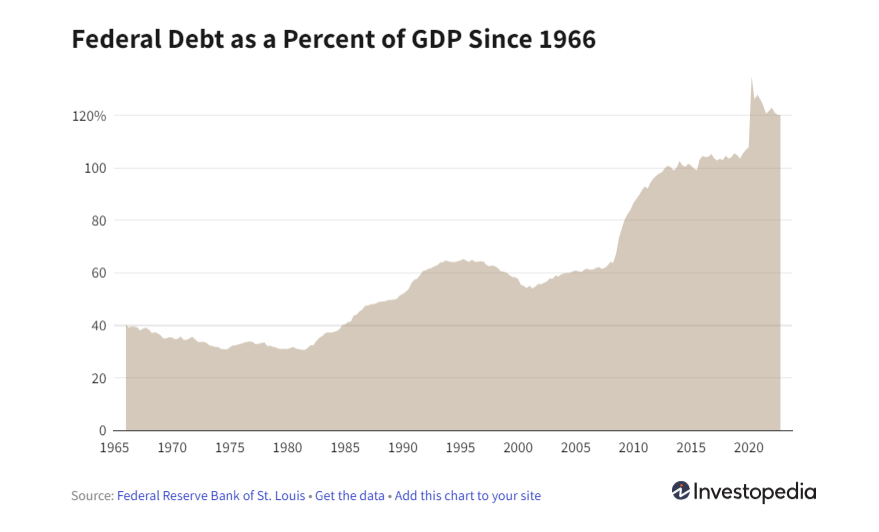

It carries a gross federal debt of $34.9 trillion. That is what we call the USG’s visible debt.

(Below the waterline, like an iceberg, is the hidden debt, promises the government has made to its citizens that are not funded. That is more than $200 trillion. Washington’s response to the hidden debt is “Never mind!” So, we’ll move on.)

The USG’s debt today is 127 percent of the nations supposed productivity, what the government calls Gross Domestic Product. Here’s a recent graphic illustration of the gross (visible) debt and its share of GDP.

Former US Budget Director David Stockman recently detailed what has gone on over the last 50 years that is reflected in the above chart: “The public debt is up 89-fold, from $389 billion to $34.5 trillion. And its share of GDP or burden on the US economy has nearly quadrupled, rising from a post-war low of 36% in 1970 to an all-time high of 122% at present.”

And to circle back to the hidden USG debt, Stockman describes their growth path as well:

“Major entitlements are on a path from 10% of GDP at the turn of the century to more than 23% by 2050. And the overwhelming share of that gain will be due to a retired population that will grow from 50 million at present to 80 million by 2050, putting huge upward pressure on Social Security and Medicare outlays.”

The bottom line is that none of these debts, visible or hidden, can be paid except by the expedient of printing money. That’s why the people on Capitol Hill seem so unconcerned. They can spend all they want, and the Fed will make it possible by creating more dollars out of thin air.

That will destroy what is left of the dollar’s purchasing power. It will destroy the middle class as well. But as they say in Washington, “Never mind!”

The Crowstrike Outage Shows How Fragile Our Digital Infrastructure Can Be

The headlines captured the story this way:

It’s like Y2K, except it happened this time!

“Largest IT Outage In History” Sparks Disruptions Worldwide!

Unprecedented IT Outage Cripples Businesses Around the Globe!

The IT shutdown impacted major banks, stock exchanges, 911 services, media, and airlines.

Here’s the lead from the financial site Zero Hedge: “Early Friday, a global IT outage caused by an issue with cybersecurity firm CrowdStrike disrupted flights, banks, retailers, stock exchanges, 911 call centers, and media outlets. Experts say this could be one of the largest IT outages in modern history.”.

The first question on many people’s minds was whether the outage was a terrorist strike or an act of war. The only good news was that it wasn’t a security incident or a cyberattack, according to CrowdStrike CEO George Kurtz.

But it could have been. It makes it a lot easier to ask, “what if,” doesn’t it?

Once again, we see just how vulnerable we are. So, what happens to your ability to access your money when the internet goes down? Or the power grid is attacked? You are stuck unless you have money like gold and silver that is off the grid.

Oh, and do we need to drive the point home by mentioning that we also just learned last week about a massive hack of AT&T records in 2022?

From NBC: “A 2022 security breach compromised the data of ‘nearly all’ AT&T cellular network customers, with hackers stealing six months’ worth of call and text message records, the company said Friday.”

Here is what we wrote in 2019 (when gold was just over $1,300!:

Some people buy gold for privacy. They would like to keep their financial affairs better protected. Since the banks have become snoops for the government, reporting what you do, and since big corporations try to follow you in everything you do and anything you buy, just the peace of mind of having a little privacy is a very good reason to own gold.

You may remember how a lot of things were shut down after 9/11. Have you even wondered what would happen if the increasingly stressed national electricity grid went down, or if solar flares screwed up satellite functions and digital communications?

What would you do if ATM machines stopped spitting out cash?

I can tell you this. In any of those circumstances you would be very happy to own gold and silver, the world’s most liquid commodities.

Visit with an experienced precious metal professional at Republic Monetary Exchange and learn about the importance of getting your wealth off the grid and into the world’s most enduring forms of liquidity, gold and silver.

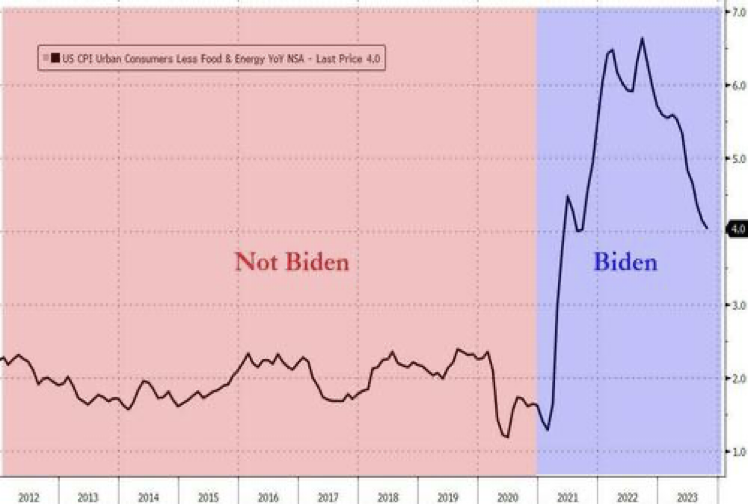

Is the Inflation Rate only the 3% that the Government says it is?

Here’s a wake-up call! Yes, another one!

The government tells us the inflation rate is currently 3.0 percent. That’s the Consumer Price Index increase for the 12 months ending in June.

Between January 2020 and last May, consumer prices rose 21.75 percent. According to government numbers, that is.

Sure. Biden is at the peak of his game. He’s never been better. And consumer prices have only risen 21.75 percent over roughly the last 4 ½ years.

Why do we find this number so incredible?

Simple. It doesn’t square with our experience or the experience of anyone we know!

One fellow posted a TikTok video showing a Wal-Mart receipt for a grocery purchase he made in 2022. The 45 items he purchased – he described it as a full month’s groceries – cost a total back then of $126.76. Because the app has a “reorder all” feature, he found that the same purchase today would cost $414.39!

Hello? Or as the fellow said himself, “Like, what?”

That’s an increase of 226 percent! In two years! For the same items!

Maybe Janet Yellen can deny experiencing sticker shock at the grocery store. She has a car and driver, and a private Fed dining room.

As off-kilter as the CPI is, the Fed prefers to use something called the Personal Consumption Expenditure Index to measure inflation. Jeffrey Tucker of the Brownstone Institute thought to ask an AI how that index is computed:

The BEA uses the same data that creates the quarterly GDP [gross domestic product] report, which measures U.S. economic output, but the PCE price index measures consumer purchases through different calculations. It converts the prices, which are still the producers’ prices, to the end price paid by the consumer. The PCE price index includes the broadest set of goods and services compared to other measures of consumer price changes. It measures changes in a basket of goods and services, but the PCE is based on data from businesses and trade organizations while the CPI is based on survey data from tens of thousands of consumers. The BEA normalizes the data via a price deflator—a ratio of the value of all goods and services produced in a particular year at current prices to that of prices that prevailed during a base year—to get the monthly PCE index: the average monthly rate of inflation (or deflation) for the U.S. economy as a whole.

Well, that’s one way to cook the books! There are others. Things like “core inflation.” Core inflation doesn’t include energy or food costs, although I’d like to see the cost of buying anything – anything at all – that doesn’t depend in some way on energy and food.

It’s all “lies, damn lies, and statistics” as Mark Twain may or may not have said. For us, the answer is to buy gold and silver to protect yourself from all the number fudging and money printing. And if you want to know what’s really happening to your cost of groceries, save your receipts.

We have shared our view that the Federal Reserve is anxious to cut interest rates before long to help elect Democrats in November. (See our January post THE FED TILTS THE SCALES! TO THE LEFT, OF COURSE!)

It’s not too complicated. The very existence of a central bank is a left-wing dream come true. It was on Karl Marx’s shot list. So, you shouldn’t be surprised to learn that there are 10 Democrat economists for every single Republican economist at the Fed.

The latest consumer price and producer price indices are somewhat contradictory, but the is ample clear evidence piling up that the economy is slowing. That will give the Fed cover for cutting rates ahead of the election.

Unemployment has begun to climb. It has reached the highest level since November 2021, while wage growth has risen at the slowest rate in more than three years.

But what about the Fed’s insistence that it would bring inflation down to 2 percent?

Fuhgeddaboudit!

Here’s the way Fed chairman Powell put things in his recent congression update on monetary policy: “Reducing policy restraint too late or too little could unduly weaken economic activity and employment.”

Powell was giving himself running room. Doug Casey says, “The Fed has effectively given up on bringing price inflation down even though the year-over-year change in the CPI remains around 3.3%, significantly higher than the Fed’s target of 2%.

“In other words, even with their crooked statistics and rigged game, the Fed has failed even to come close to their inflation target. It’s a massive failure.”

Evidence of slowdown:

To repeat: a slowing economy and rising unemployment give the Fed the cover it needs. Many Fed watchers are now expecting two rate cuts in short order, before the election for sure, and less likely in our view, one even as early as this month. The price of gold seems to be confirming that view as it raced up to $2,400 on the unemployment news.

Bear in mind, too, that gold has climbed to new highs despite the Fed’s higher interest rate regime. Now imagine what happens when the Fed forces rates lower, buying government bonds, and printing money to do so.

So, a slowing economy, more money printing, rising gold. Sounds like the stagflation decade all over again!

Your Essential Financial Survival Briefing! The American Gold Story!

Reviewers praise Real Money for Free People!Rich Dad Poor Dad’s Robert Kiyosaki says Jim Clark’s book is “essential reading for anyone who values their financial freedom.”

New York Times bestselling author Charles Goyette says Jim Clark’s book “explains in easy-to-understand terms what the Founders knew, that honest money- gold and silver- means prosperity and freedom for both nations and individuals.”

Skyrocketing prices, massive new spending programs, debt ceiling puppet shows, money printing, debt up the wazoo!

How did we get here? Where is all this headed? Here’s an excerpt:

Our governing classes and monetary authorities] have created the conditions for an explosion of impoverishment. They are the big spenders and reckless borrowers of both parties. They are the grand councilors and academic advisors of the almighty State. They and their statist epigone and media servitors are the inevitable offspring of connivers like Franklin Roosevelt and Richard Nixon, who stole the people’s gold and betrayed the nation’s good-as-gold dollar…

There is no turning back. They must now continue to print money until the system crashes. It is the endgame of their folly.

REAL MONEY FOR FREE PEOPLE is a fast-paced review of why the Founding Fathers, to assure a free and prosperous America, built the new republic on a solid monetary foundation of gold and silver. Learn how later politicians, those of lesser character, have abandoned that foresight by handing America’s future and prosperity over to self-serving bankers and money manipulators.

In this book, Jim Clark pulls back the curtain to reveal what the mainstream media conceals: how the unsustainable and reckless policies of the Federal Reserve are destroying the dollar and your savings.

More importantly, it tells you exactly why gold and silver – the world’s most treasured and time-tested forms of money – are your key to protecting your wealth and profiting in the years ahead!

NOW AVAILABLE FOR THE FIRST TIME ON AMAZON.COM! Click Here!

With this post, we hope to show you how seriously the rest of the world takes gold in this new era of de-dollarization.

The following bullet points are taken from an article by Sergei Glazyev, Commissioner for Integration and Macroeconomics within the Eurasian Economic Commission and a close Putin advisor, which appeared in Vedomosti, the Moscow business paper in December 2022.

Our thanks to Alasdair Macleod for providing this translation on his Substack page. Macleod stresses the importance of these remarks given the US sanctions and asset grabs and Russia’s presidency this year of the BRIC nations and as background for the major BRICs meeting coming up in October.

The sanctions imposed against Russia boomeranged on the Western economy. The geopolitical instability they provoked, rising prices for energy and other resources, inflation, and other negative factors put strong pressure on the global economy, in particular the global financial market.

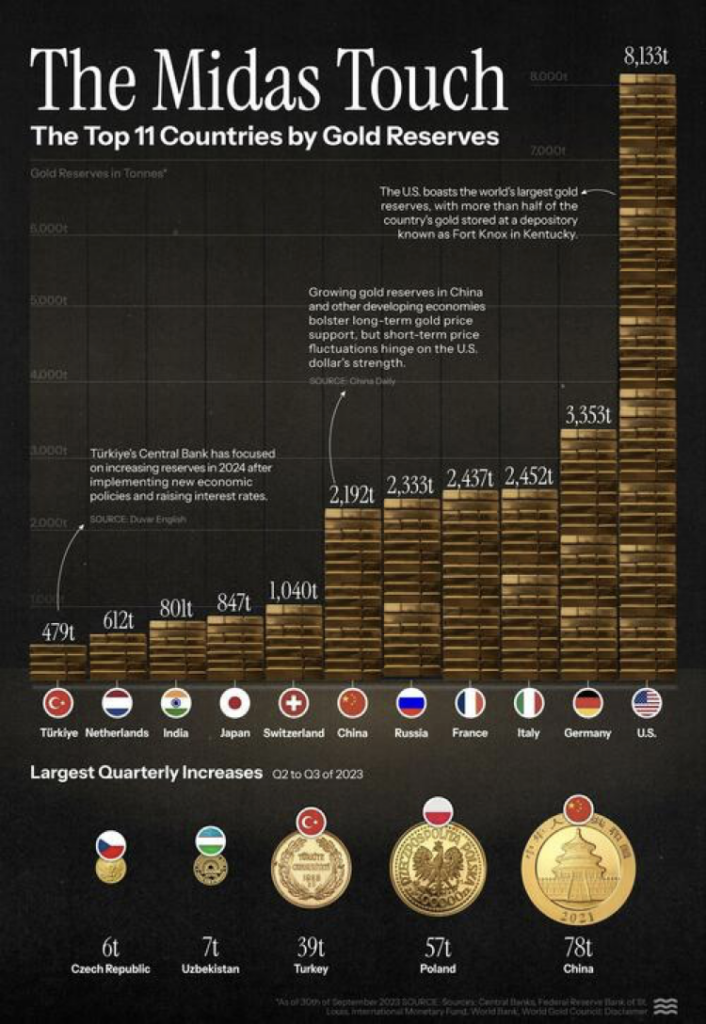

Large gold reserves allow Russia to pursue a sovereign financial policy and minimize dependence on external lenders. The amount of reserves affects the country’s reputation, its credit rating and investment attractiveness…. In 1998, the lack of sufficient international reserves became one of the causes of the crisis, which ended in default for Russia. Now our country already has large gold and foreign exchange reserves, being fifth in the world (after China, Japan, Switzerland and India) and ahead of the United States. But this is not enough.

Over the past quarter century, gold has been flowing from West to East through the main hubs (London, Switzerland, Turkey, the United Arab Emirates, and others) with a capacity of 2000 – 3000 tons per year. Did the western Central Banks’ official gold reserves remain in their storage facilities? Or has it all gone through swaps and leasing? The West will never say, and Fort Knox’s audit will not.

Over the past 20 years, gold mining in Russia has almost doubled, while in the United States has almost decreased by half. By dismantling real wealth, the United States has lost its competence and interest in the production and processing of strategic resources (gold and uranium, etc.). The printing press funds the purchase of everything they want.

The world financial order has tolerated the printing press dollar since the end of World War II. But the post-war order is coming to an end and the pace of de-dollarization will accelerate dramatically. The dollar will eventually end up the “Old Maid.” No one will want to be holding it when the game ends. Prepare your own future accordingly.

They’re even wrong about being wrong about inflation!

What a bunch we have running fiscal policy in our country. Treasury Secretary Janet Yellen has distinguished herself for being wrong about inflation and virtually everything else. And President Biden, well there’s no need to describe his abject confusion anymore. Since everyone except a few shameless toadies in the media can see it, that would be beating a dead horse.

But their public positions are both utterly incoherent and incompatible. When fiscal policy is this contradictory, it is time to seek refuge in gold and silver!

Yellen’s cluelessness and apologies for not understanding inflation are the stuff of legend. But there is more, so much more…

Her support for a wealth tax, a tax not on income but on property people own, a tax on unrealized capital gains that would even require people to sell family businesses to pay, would have Karl Marx dance a commie jig!

Equally destructive was her support for the administration’s crazy desire to have banks report people’s every transaction of $600 or more. Imagine how utterly mentally vacant she must be to not have envisaged how much strangling bureaucracy that would have created. Inconceivable!

Her failure to have the Treasury issue long-dated bonds before the Fed began raising rates is just one more component of our debt disaster. Stanley Druckenmiller calls this “the worst mistake in the history of the Treasury.”

Then there is her assertion that the US can afford two wars at once. “Absolutely!” she says. That was eight months ago when the national debt was $33.56 trillion. Today it is $34.68 trillion. Up well over a trillion dollars in eight months!

As for Biden, just as he wanders, squats, and mutters aimlessly at photo shoots, shadowed by handlers trying to cover for him, he bats about for something to say about inflation until he comes up with something his handlers prepared for him. Bill Bonner describes him similarly: “Biden, the man, is just a cut-out… a place-holder. We’ve never heard an original thought pass his lips, nor an insight worth remembering. Instead, his pensée is just much-rehearsed blah-blah, sticking with whatever talking points his handlers suggest.”

So, what has his people had him saying about inflation? Greed, of course.

But greed has always been with us. If greedy corporations are responsible for inflation, if they have the power to unilaterally raise prices, why wasn’t inflation out of control before Biden? (Note that Washington never blames inflation on government greed! It never points to all the money it shovels to its cronies and its favored interest groups. It is never, ever about their greed).

But in any case, Biden and Yellen are not even able to keep their stories straight! The other day on CNBC Yellen contradicted Biden’s attribution of inflation to corporate greed. “I think that inflation is about supply and demand,” she said.

Well, of course, all prices are about supply and demand. When the government prints trillions of dollars out of thin air and distributes them to its friends, they increases demand. Same amount of goods and services in the economy, but suddenly some people have a lot more printed money with which they buy things. It’s like an auction: they are bidding prices higher and higher.

The cluelessness is not limited to just Biden and Yellen. It is systemic in the administration and, frankly, in both parties and throughout Washington and the governing classes. Take for example the cluelessness of Jared Bernstein, the president’s chief economic advisor, about how monetary policy works. See for yourself:

The ship of state is being run by the intellectually deficient. It is a ship of fools. They are incapable of steering us out of a currency storm. They will destroy the dollar and leave your prosperity wrecked upon the reefs.

The need to own gold is growing more critical by the day. Because something will happen!

It is our view that the mainstream media ignores or underplays the significance of all of the forces destroying our currency and prosperity. But it seems most clueless about the way war destroys both. However, our hands-on experience goes back a long way. We remember the Vietnam War and the role it played in ending the gold-backed dollar, just as we remember the Soviet invasion of Afghanistan, the revolution in Iran, and the fire they lit under gold prices.

So, we are not willing to turn a blind eye to war drums beating today. We note that the situation in Ukraine is escalating with the attack on Sevastopol, Crimea. Russia blames the US and promises to retaliate. The widening of the Mideast war to include Lebanon is another fuse that appears about to be lit.

DE-DOLLARIZATION

The move away from the dollar and to gold is very real and a key driver of higher gold prices. It can only accelerate. Note for example that a Russian court has approved the seizure of hundreds of billions of dollars of assets from Western banks, a response in kind to the theft of Russian assets by the sanction regimes. It goes without saying that this makes dollar-holders around the world very nervous indeed and heightens gold’s allure as an asset whose value is not subject to the whims of some issuing government.

INFLATION

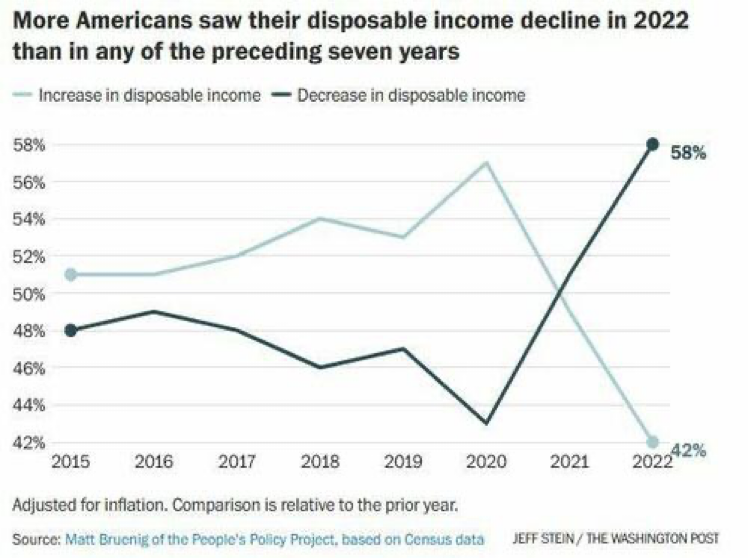

Inflation teaches everyone that eventually made-up government money loses value. The highest US inflation in more than 4o years is beginning to drive that lesson home. Average weekly earnings have risen over the last 3 ½ years, but rising prices have undone any advantage, as the average real (constant dollar) income of working families has fallen $2,300.

Some get it already, but eventually, almost everyone will realize that this is not because of cosmic rays or the greed of corporations, but because the money itself is being managed specifically to lose purchasing power. Then what can today be called a slow diversification by some Americans into gold and silver will become a stampede.

DEBT

All inflations are the result of dishonest governments spending money they do not have and running up debts that they cannot repay.

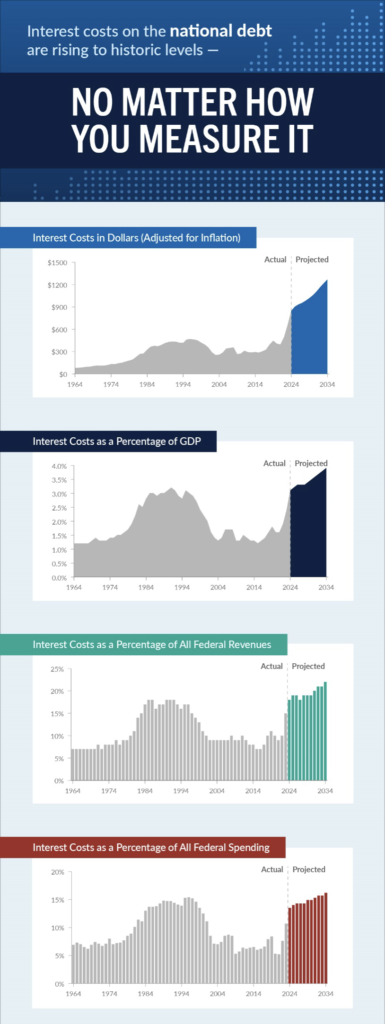

Even the Congressional Budget Office, which tries its best to downplay the real debt debacle, expects the budget deficit to skyrocket, from $1.9trillion this year to $2.8 trillion by 2034.

As for the national debt itself, it will hit $35 trillion in a few weeks, and $37 trillion by the end of this year. In fact, on our current path, the debt will reach a stratospheric $60 trillion at the end of the ten-year budget window, according to David Stockman. And that, he adds, is with the happy face the CBO is putting on its projections:

Even that depends upon the latest CBO iteration of Rosy Scenario, which envisions no recession ever again, just 2% inflation as far as the eye can see and real interest rates of barely 1%. And that’s to say nothing of the trillions in phony spending cuts and out-year tax increases that are built into the CBO baseline but which Congress will never actually allow to materialize.

David Stockman

So, there you have the four biggest drivers of higher gold prices now and in the foreseeable future: war, de-dollarization, inflation, and debt. All four are hopelessly intertwined, each powering the others.

Other less visible developments will add to the fuel-propelling gold higher, little-noticed financial annoyances like the war on cash and major destructive forces like the unstoppable spread of state socialism.

Don’t wait any long to protect yourself, your family, and your wealth with gold and silver.

If it is so strong, why does it buy less and less?

Headline, the Wall Street Journal, June 4, 2024: The Dollar Is at Its Strongest Since the 1980s. Can It Last?

Sorry, but it’s flapdoodle. Gobbledygook. Gibberish. Bafflegab.

Or to put it in more serious terms, it’s Newspeak.

George Orwell coined that term in his uncannily prescient novel 1984. Newspeak is a language of simplified grammar and limited vocabulary designed to narrow the range of critical thinking.

The WSJ provides a caption to a photo in its “strong dollar” story: “The U.S. dollar has defied analysts’ expectations and appreciated again this year relative to a basket of other currencies.”

It should have said “The U.S. dollar depreciated again this year relative to a basket of groceries.”

The WSJ can get away with calling it a strong dollar because they are a financial newspaper. And it is true that if you are importing Mercedes, the exchange value of the dollar matters. Chances are if you are importing foreign goods, or exporting US goods, you are very much aware of currency differentials and that you are hedging them when you need.

But for the sake of clear communication, the term “strong dollar” should go in the deleted file. Especially since most of us at any given time aren’t importing Mercedes.

The financial press gets away with it as a sort of faux sophistication: “Our readers know what we mean!”

Some do. But the real damage is done when the rest of the financially clueless media pick up on it. So, the rest of then repeat ad nauseum on talk shows and general newscasts that the dollar is strong. The people who hear that pass it on in conversation at work or to their neighbors.

But even the financial press should be careful not to sound like toadies of the government. After all, they don’t say Tesla was “strong” today or Ford was “weak.” They say those stock prices are up or down, higher or lower.

To call the dollar strong is wildly misleading. The dollar can only be said to be strong when compared to other currencies that are constantly losing real value. The WSJ story came hard on the heels of Mexico electing some hard leftist president. Her father was a communist and it is not clear where she differs from Karl Marx. Because people like her destroy wealth and ruin currencies, the Mexican peso immediately fell, down as we write about 9 percent. A peso down would mean the dollar, comparatively speaking, is marginally higher. But because Mexico elects a socialist (more trouble on our southern border!) the dollar is strong? Don’t kid yourself!

If currencies were ships, and Mexico’s ship was sinking at a nine percent rate and the US ship was sinking at a 3 or 4 or 5 percent rate, would you say the US ship is seaworthy?

The dollar isn’t strong at all. It is weak. Extraordinarily weak.

That is because the function of a currency is to allow people to purchase things. With that in mind, here is a 10-year chart of the US dollar’s purchasing power:

It doesn’t look particularly “strong,” does it?

Nevertheless, they say, “the dollar is at its strongest since the 1980s.” When it bought a heck of a lot more than it does today.

So, when you hear the media tell you the dollar is strong, you’d better compare it to something real like the price of gold.

Those who do that are thinking for themselves despite the media’s Newspeak. And they are buying gold.

Here is just a short list of the major – some might say existential – threats we Americans are facing.

They all have the same cause. It’s not hard to figure out. It‘s not because of the alignment of Jupiter and Mars. It’s not because of subversion by space aliens.

They are all caused by Washington and our growing left-wing national ethos.

All of them.

Here’s a rundown.

Our lifespans appear to be growing shorter. “The numbers are shocking.”

Harvard School of Public Health, April 13, 2023 – U.S. life expectancy has declined to 76.4 years, the shortest it’s been in nearly two decades, according to December data from the CDC….

[Dean Michelle Williams] noted that younger people in America are dying at higher rates than their counterparts in other high-income countries and that the U.S. also has among the highest maternal and infant mortality rates among upper-income countries.

American IQs are falling. “The first time ever.”

The New York Post, May 3, 2024 – A report from 2023 revealed the depressing reality — that the average intelligence test score fell from 100 to 98, a dismal, two-point decline after a previously uninterrupted 30-point rise that began in 1905.

American public schools are a national disgrace. “In public education, we reward mediocrity and discourage excellence.”

The Discovery Institute, July 11. 2023 – Detroit Public Schools [are ranked] the worst performing of all 26 large city districts, with just 5 percent of their eighth-grade students rated proficient in reading and only 3 percent in math. What is surprising is the Detroit Public Schools Community District rated 99 percent of Detroit’s teachers as “highly effective” or “effective,”

Teacher[s] cannot be fired for poor performance. Consequently, evaluations have little or no meaning. Not only can teachers not be fired, but incompetent teachers will make more money next year as they gain another year of seniority and an automatic raise.

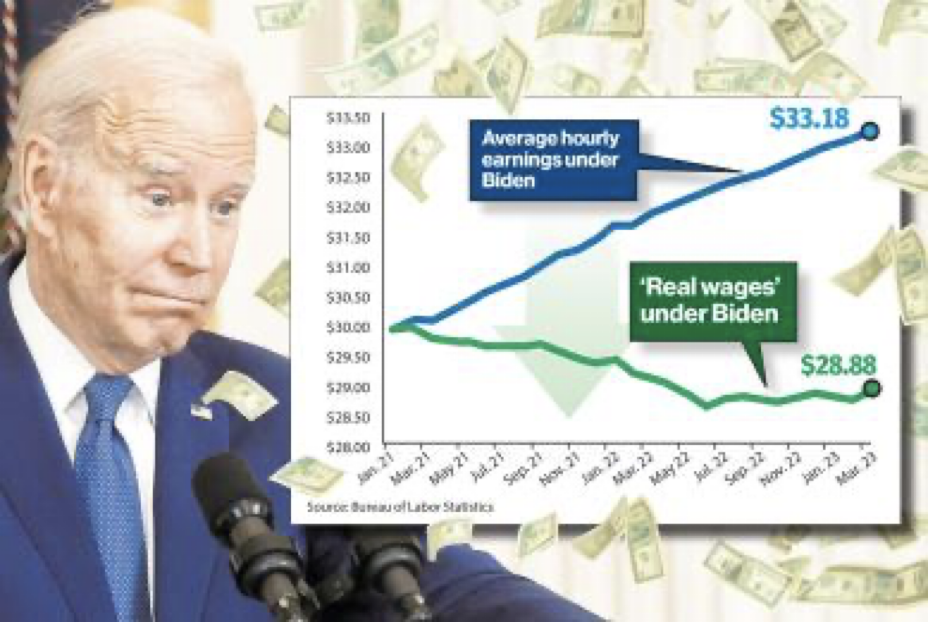

The American Dollar Is Worth Less Each Year – “Inflation hits 20 percent under Biden.”

The Hill, May 15, 2024 – Inflation under President Biden hit a cumulative 20 percent. The dollar’s value has plummeted under his watch. The Bureau of Labor Statistics also confirmed that the consumer price index is resurgent and growing faster than average wages. Combined with weak GDP growth, this data shows the U.S. economy is reentering stagflation.

You can’t personally do much about most of these problems. Crowded hospital waiting rooms and strained facilities can be your problem in an emergency. You can be victimized by falling IQs and failing schools if underqualified candidates are made airline mechanics, air traffic controllers, or are given a host of other jobs.

And you can’t possibly do much about America’s economic destruction. Millennials are expected to be the first generation to earn less than their parents. Two of three middle-class respondents say their income is falling behind the cost of living.

But you can do something – and do it at once! – about the collapse of the US dollar’s purchasing power.

It’s like emergency medical workers performing triage: They sort out and prioritize the injured. What must they immediately treat? What comes first?

In the case of these existential crises, the first and more urgent problem that can be addressed immediately is to protect yourself from ongoing currency failure. You can insulate yourselves from the criminal mismanagement of the dollar, its quantity and quality, by investing in gold and silver. Both have records of superior performance as money that goes back thousands of years.

Speak with a Republic Monetary Exchange precious metals professional. He can help you achieve the protection you need in the days ahead.

Brace yourself! Another huge wave of inflation is approaching! The purchasing power of your savings is about to get swamped once again.

So far the purchasing power of the US dollar has lost about 20 percent of its value during the Biden presidency. But the Biden presidency is not over yet! Brace yourself for more Biden inflation and brace your savings with gold and silver.

The gold and silver markets are saying another wave of inflation is about to hit!

Here’s what is going on:

Wholesale prices are running hot. The Bureau of Labor Statistics reported recently that the Producer Price Index accelerated to its highest level in a year. Producer prices are a leading indicator of coming consumer prices because producers pass along their higher costs. Stated differently, today’s wholesale prices are tomorrow’s consumer prices.

Rising commodity prices mean higher consumer prices, too.

Copper is one of the leaders in rising commodity prices, but others include coffee and chocolate, coal, natural gas, soybeans, wheat, coal, milk, orange juice, and butter.

Reporting that the Commodity Research Bureau index just hit its highest level in 13 years, the Committee to Unleash Prosperity remarks that “anyone who thinks we have turned the corner on Bidenflation – and we know that includes at least half the economist in Washington – should have their head examined.”

Get ready for another wave of Biden inflation and for the purchasing power of your savings to fall even more.

Don’t get caught. Make sure to protect yourself with gold and silver. See us now!

Suppose a hundred years ago some far-sighted benefactor, someone a few generations back, wanted to leave some wealth for their descendants – including you. Would you be better off if they left you $10,000 cash in bills or $10,000 in gold?

A hundred years ago American money was gold. Americans commonly carried and conducted commerce in $20 gold pieces. They were the coins of the realm. But if you thought carrying them around – especially in great quantities – was inconvenient, you could use paper money. A US $20 note issued by the Treasury was just a claim check or a warehouse receipt for gold. If you wanted to, you could walk into any bank or go to the Treasury and exchange that paper $20 note for real gold. No questions asked.

So your benefactor would have had a choice. Which would you have wanted then to leave, paper or gold?

You probably don’t have to think about it too hard. The US paper dollar has lost about 95 percent of its purchasing power since 1924.

Someone naïve argued about that with us once. “That’s impossible,” he said. But figure it out for yourself. Inflation officially reduced the dollar’s purchasing power by 3.4 percent last year. It reduced it by 6.5 percent in 2022. And so on, year in and year out.

Here’s a shortcut. Consumer prices are up about 20 percent since Biden was sworn in. That means today’s dollar only retains 80 percent of the purchasing power it had in January 2021.

Add in more than a few years of year-after-year inflation along the way, and soon you will find that the loss of purchasing power really adds up!

If a thief broke into your bank account and stole 3.4 percent of it last year and 6.5 percent of it the year before and has been stealing from it every year of your lifetime, you might be upset. You might call the authorities. But there is no point in calling the authorities on what is happening to the dollar because it is the authorities who are doing it!

The $20 gold piece contained just a little less than an ounce of gold, at exactly .9675 ounces. Based on a recent gold price of $2,350, just the gold content of a $20 gold piece would be $2,274 ($2,350 x .9675 = $2,274).

So the price of gold has increased close to 113 times ($20 x 89 = 2260)! Think about that in percentage terms. Your gold has increased by 11,300 percent! That’s an average of 113 percent a year!

(The story is even better than that because, thanks to their rarity, desirability, and for other reasons, investors and collectors prize those beautiful U.S. gold coins beyond just their gold content. Ask your Republic Monetary Exchange gold and silver professional about this.)

As for the paper money? Well, it lost most of its purchasing power. That is the common fate of unbacked paper money throughout time.

So by now, even if you had never thought about our question before, you will have doubtlessly concluded that you would have wanted your would-be benefactor a hundred years ago to leave you real gold instead of paper money.

Our story says something about real money and wealth preservation in this day and age.

That’s only part of the story, that honest precious metal currencies hold their value. So with the clear interest that the people have in a reliable form of money that holds its value, why do governments hate gold and silver money? Why is it that the more dishonest and corrupt they are, the quicker they turn to printed or digitally printed money?

That, as they say, is the rest of the story. We’ll write more about that one of these days, but if you’d like to cut to the chase and get the answer to that and your other questions about wealth preservation, speak with a Republic Monetary Exchange precious metals advisor today!

To us, the real estate bubble was blindingly obvious. That is why we tend to keep an eye on those who also saw it coming. Ron Paul is a case in point. Not only did he see it coming, he famously explained in Congress and in detail exactly how it would unfold.

And so it did.

Now two important figures in the investment world who made their chops (and untold millions of dollars) calling the housing bubble back then are turning to gold.

Michael Burry and John Paulson. A new Business Week article says, “Michael Burry and John Paulson hit the jackpot when they called the housing crash. Now they’re betting on gold.”

Michael Burry was made famous in the movie about the bursting of the mortgage bubble, The Big Short.

Burry, who was played by a scruffy-looking Christian Bale in the movie, made himself and the investors in his fund hundreds of millions of dollars by shorting mortgage credit instruments.

Burry was also on our radar screen in 2022. While the Fed was patiently explaining transitory inflation, Burry was tweeting furiously about inflation on our doorstep. He was right and the Fed officials have been making excuses ever since about the highest inflation in more than 40 years.

John Paulson is the head of Paulson & Co., a major investment firm. He made billions by spotting the housing bubble in 2007. Wikipedia says he made another $5 billion in 2010 primarily investing in gold.

About a year ago we cited Paulson in these pages on global de-dollarization: “There has been a significant increase in demand from central banks to replace dollars with gold, and we’re just at the beginning of that trend. Gold will go up and the dollar will go down, so you’d be better off keeping your investment reserves in gold at this point.”

Good call, John!

Now to keep you up to date, Business Week reports that Burry has placed an $8 million stake in gold. And after examining his firm’s SEC filings, Business Week tells us that Paulson also has big bets on gold.

As Paulson told an interviewer last year, “We’re at the beginning of trends that are going to increase the demand for gold, and inflation and geopolitical tensions will determine the rate at which gold increases. This year gold will appreciate versus the dollar, and also over a three, five, and ten-year basis.”

We don’t want any of our friends and clients to miss out!

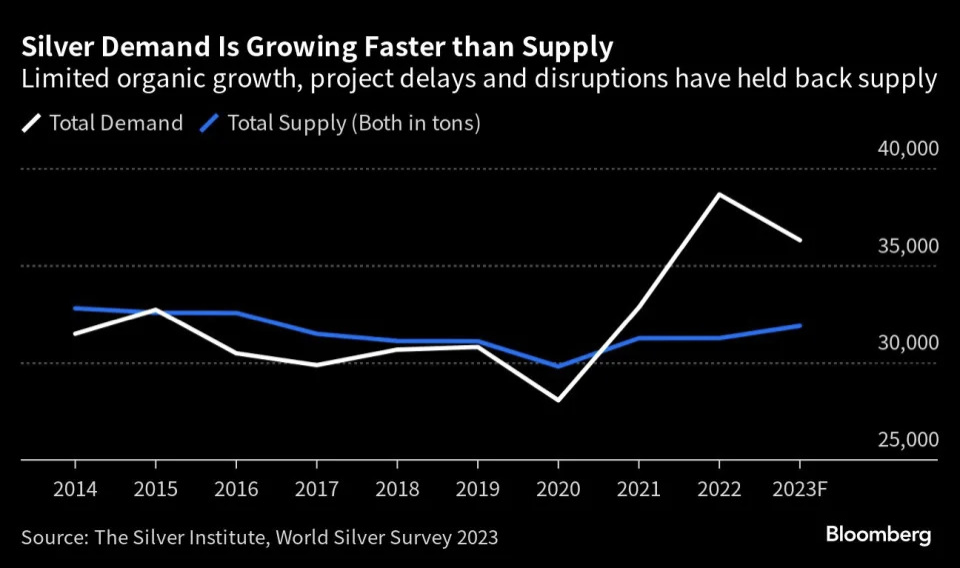

Everywhere you look, commodities are screaming higher and higher. Gold, coffee, chocolate, uranium, copper, nickel. And silver!

But nowhere in the commodity complex is the opportunity greater than in silver! Try taking delivery of investible quantities of chocolate and storing it for years to come. How about uranium? Now there’s a real liquidity problem.

Yet silver checks all the boxes. It is among the most liquid and widely traded commodities, perfect for individual investors. When you buy silver of .999 percent purity, the standard for investment bars and most coins, you don’t have to have the silver assayed when you choose to sell. Good luck with liquidity for investment-grade quantities of coffee.

Silver has a history of thousands of years as a monetary commodity. In fact, silver has been used as money longer and in more places than gold itself.

At the same time, its industrial use for things like electronics and photovoltaics grows every year. Silver industrial demand rose 11 percent last year. And last month silver stockpiles tracked by the London Bullion Market Association fell to the second-lowest level on record.

As we write this, gold prices are up 17.5 percent year-to-date while silver has surged by 35 percent during the same period!

With that move, silver remains at bargain prices. It is still way below its all-time highs. Silver was $50 an ounce in 1980. That was 44 years ago. Are there any other major industrial commodities that are 40 percent below their price of 44 years ago? Don’t kid yourself!

Silver reached highs of about $50 in both 2011 and 2012.

Lately, our radio messages and blog posts have focused on alerting our friends and clients about the opportunites unfolding in the silver market.

Want to learn more? Just pick up the phone and call 602-633-8315 to speak with a precious metals expert anytime Monday through Friday, from 9 AM-5 PM MST!

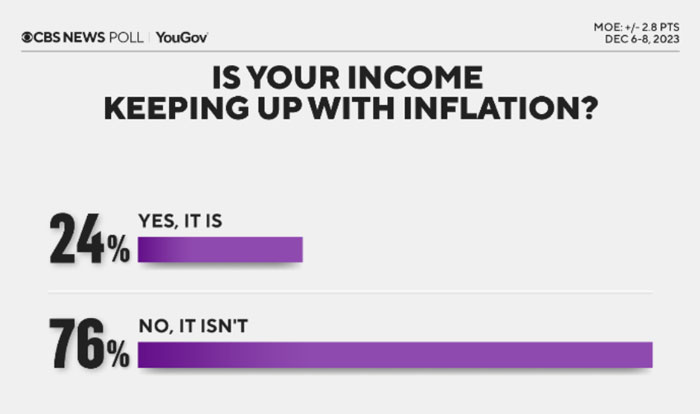

The headline on Yahoo! Finance reads, “Living on Edge: Nearly 90% of Retirees Worried Inflation Will Eat Away Savings.”

The story reports that a third of retired Americans are worried that they haven’t saved enough. No surprise there. 89 percent describe themselves as deeply concerned about the erosion of their purchasing power by inflation. As well they should be. You can not reply on a dollar-dependent retirement.

Add to that a crisis of confidence over the future of Social Security. 44 percent of non-retired Americans are afraid that Social Security will run out.

Will it run out? It already has run out! The money you and millions of Americans paid into Social Security over your lifetime has been spent. In its place, the politicians left an IOU.

Great. A government that can’t even pay its on-the-books visible debt of almost $35 trillion is whistling past the graveyard if it is pretending that it can pay its off-the-book hidden debts like Social Security. Those hidden liabilities, conservatively estimated, come in at about $215 trillion – more than 6 times more than the already unpayable visible debt.

That is why we say don’t even think about a dollar-denominated retirement!

Consumer prices are up 20 percent – at least – since Biden became president. We say at least because except for ever-changing statistical modeling price gimmickry, the inflation rate would be much, much higher. John Williams at ShadowStats.com continues to track the inflation rate on the same statistical basis that prevailed before sketchy “hedonic” adjustments were figured in. On that basis, the real inflation rate is 8 percent, which certainly tracks much closer to the real-world experience of families today. An 8 percent inflation rate doubles the cost of consumer goods in just 9 years. Try to maintain a retirement budget with that going on.

Let us illustrate the point one more way. Between December 2019 and March 2024, the Bureau of Labor Statistics says the CPI increased by 21.5 percent. How much has the price of a Big Mac gone up in the same period?

87.7 percent.

If we have made the point clear that one should not even thing about trying to survive a dollar-dependent retirement, we recommend you make an appointment with a Republic Monetary Exchange gold and silver professional to discuss a plan to prepare for the monetary crisis ahead with the world’s most enduring, most prized, and most desirable forms of money: gold and silver.

It’s not something that people generally want to talk about – widespread civil chaos, lawlessness, and social collapse.

But it goes hand in hand with the failure of the monetary system. And it doesn’t take a Nostradamus to see the sign of something like that on the horizon.

Just the other day we noticed that hedge-funder Ray Dalio, the founder of Bridgewater Associates, is noticing the same things. Dalio told the Financial Times that he sees a 35 to 40 percent chance we incur a civil war.

“We are now on the brink,” he said.

The publishers’ description of the book The Next Civil War: Dispatches from the American Future reveals that the battle plans for the next civil war have already been drawn up. “Not by novelists, but by colonels.”

In times of chaos, the governing authorities will do anything to keep themselves in power and to expand their power. Under cover of calamity, governments do all kinds of unthinkable things and invoke unimaginable tyrannical powers. They will target your wealth, bank and retirement accounts, and your property.

But this discussion provides a good opportunity to reiterate that your core position in both gold and silver should consist of real metals in your possession.

Ron Paul believes that the developing economic crisis, the ending of the dollar’s global reserve status, unpayable debt, and the Fed printing money to cover the Washington scoundrel’s spending will be the triggering event for what many expect is coming.

“This will result in massive public unrest potentially resulting in violence, the rise of authoritarian movements on the left and right, and increasing authoritarianism,” says Dr. Paul.

Providing for yourself and your family with gold and silver in a period of lawlessness and economic chaos is essential. A Republic Monetary Exchange precious metal expert can help you review and structure your portfolio for the fraying of social order.

It’s not good when you get three stories like this all lined up in a row, all at once on a major new site.

It’s like getting three cherries in a row on a Las Vegas slot. Except that it’s not a jackpot. Quite the opposite. Still, bells and alarms should start clanging and you need to take notice.

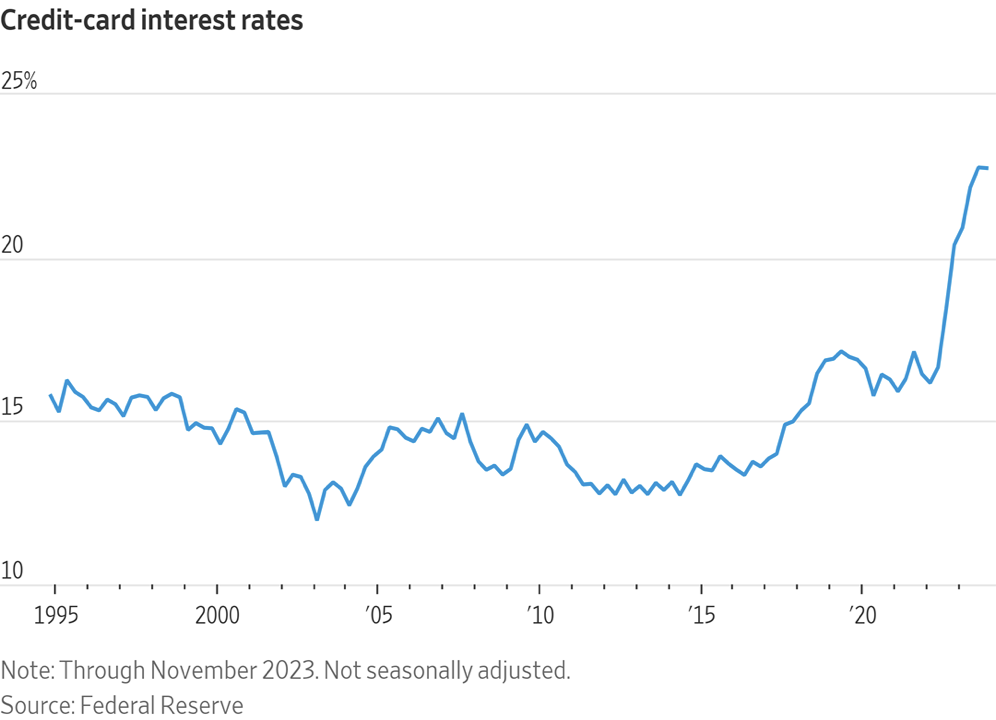

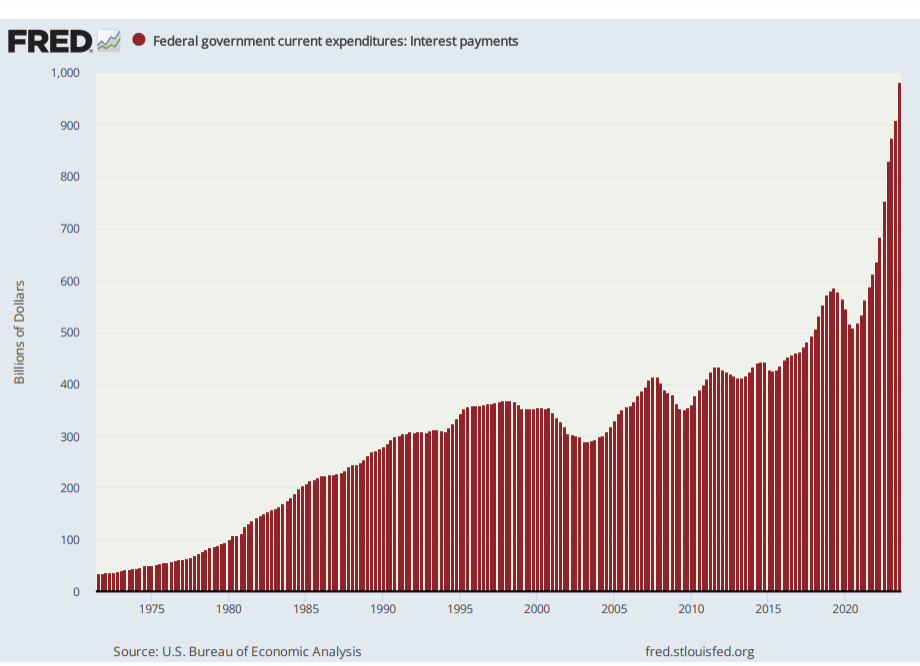

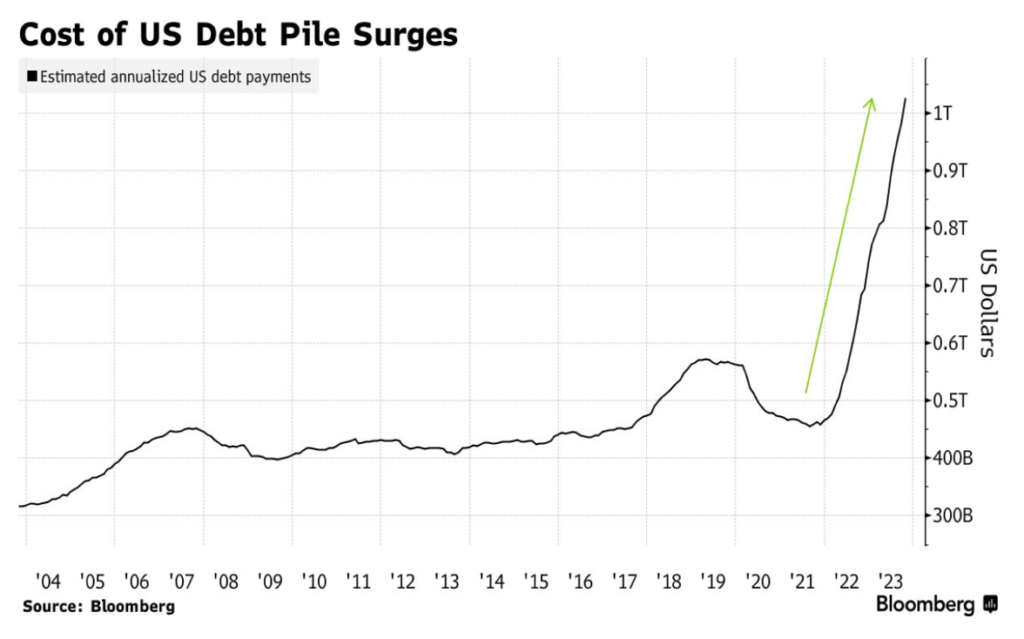

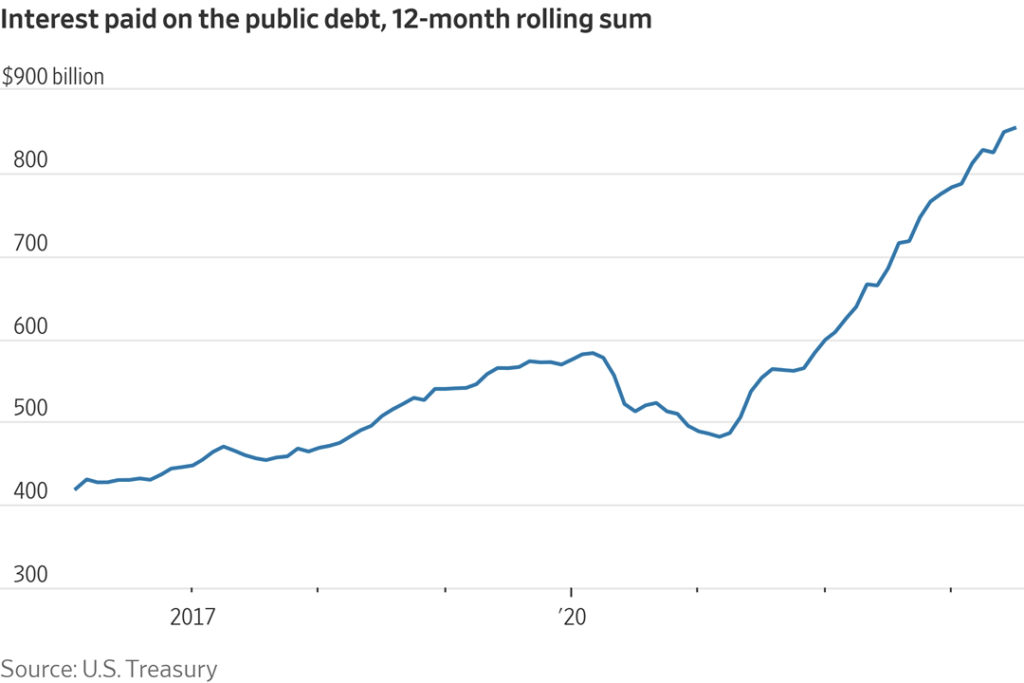

The other day all three stories lined up on the Drudge Report. First of all, higher interest rates are costing the US Treasury a lot of money. This story details that the Treasury spent $89 billion in interest payment to bond holders just in the month of March. In case you wonder how much that is per minute, a Yahoo News headline spelled it out for us: “At $2 Million Per Minute, Treasuries Mint Cash Like Never Before.” The financial press can spin it as a good thing that investors are getting interest income, but it will all be paid for by higher inflation since the government continues its wild deficit spending.

Speaking of inflation, next came the news from Business Insider that even people with six-figure incomes can’t seem to get ahead. “Inflation is scrambling Americans’ perceptions of middle-class life,” it said. The story reports that things that used to bc a part of middle-class America life appear to be ending. Half of Americans don’t plan on taking a summer vacation because of the higher cost of living, while 38 percent says they wouldn’t be able to handle an unexpected expense of $1,000 or more.

While we’re digesting all that, we get more news that makes clear that the dollar isn’t what it once was. What was it once? Once in was as good as gold. No more. Today only gold is as good as gold, as China has figured out: China Is Buying Gold Like There’s No Tomorrow first appeared on the New York Times webpage. It reports on what we have called the biggest financial megatrend of our age, de-dollarization: “In March, the People’s Bank of China added to its gold reserves for a 17th straight month. Last year, the bank bought more gold than any other central bank in the world, adding more to its reserves than it had in nearly 50 years.” (Update: New numbers just in for April: China has now been adding to its gold reserves 18 months in a row!)

So there you have it, three back-to-back stories that are all related. The Treasury is spending like crazy to borrow money it needs to stay afloat, the middle-class is in the crosshairs of the inflation squeeze, as it always is, and the world is turning to gold, as it always does.

Ding! Ding! Ding!

We think the way things are lining up, you should be hearing alarm bells. This is the time to make sure you have all the gold and silver you need for the crisis that is now underway. A Republic Monetary Exchange precious metals professional can help you construct a portfolio for safety and profit.

You just can’t turn a $24 trillion economy over to someone a clueless as Joe Biden and expect things to go well.

How many examples do you need? It was just last week the President claimed that inflation was 9 percent when he took office, but he got it on the run.

Not even close!

The big Biden lie was too much even for in-the-bag media outlets like CNN and the Washington Post which had to set the record straight. To wit:

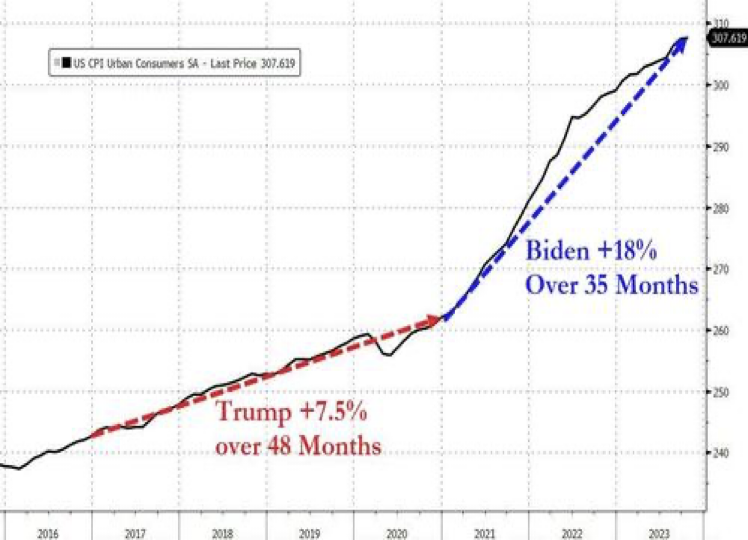

Inflation was 1.4 percent when Biden took office. It raced to a 43-year high of 9.1 percent in a year and a half.

You just can’t entrust a $27 trillion economy to someone like Biden and expect a financial crisis to be averted.

A couple more examples?

Okay:

Biden wants to drive people out of internal combustion engines and into electric vehicles. But at the same time, as analyst Michael Shedlock puts it, “Biden wants EVs so badly that he will quadruple tariffs on them.” That makes a lot of sense. The same kind of sense that in a housing affordability crisis, Biden slapped tariffs on Canadian lumber. So, are we surprised that lumber prices have risen 32 percent?

You just can’t turn a $27 trillion economy to someone like Biden and expect a financial crisis to be averted.

You’ve probably seen this video of Jared Bernstein, the Chairman of the Council of Economic Advisors. If you haven’t, please watch it and share it with everyone you know. Bernstein is utterly confused about how US monetary policy works. He is Biden’s chief economic advisor.

If the blind lead the blind both shall fall in a ditch.

You just can’t turn a $27 trillion economy to someone like Biden and his advisors and expect a financial crisis to be averted.

You cannot trust a monetary system run by these clueless people. Gold doesn’t need a Chairman of Economic Advisors. Its value is intrinsic and enduring.

Ron Paul says, “Massive public unrest… violence… authoritarianism!”

Make sure you have plenty of gold and silver, because it’s not going to be pretty!

No one has a better track record than former Congressman and presidential candidate Ron Paul when it comes to foreseeing the results of government interventions. Whether it is foreign policy like the Iraq war and the other regime change calamities, or economic like the housing bubble and inflation.

Now Dr. Paul is warning about the next economic crisis.

“Disappointingly, but not surprisingly, Congress was too preoccupied spending billions more on military aid for foreign countries and banning TikTok to pay attention to the looming bankruptcy of the two largest federal entitlement programs,” says Dr. Paul. “Many in Congress no doubt believe they can ignore the impending bankruptcy of Social Security and Medicare because they can count on the Federal Reserve to do the ‘dirty work’ of cutting real benefits and raising taxes. This result can be produced via the hidden, and regressive, ‘inflation tax.’”

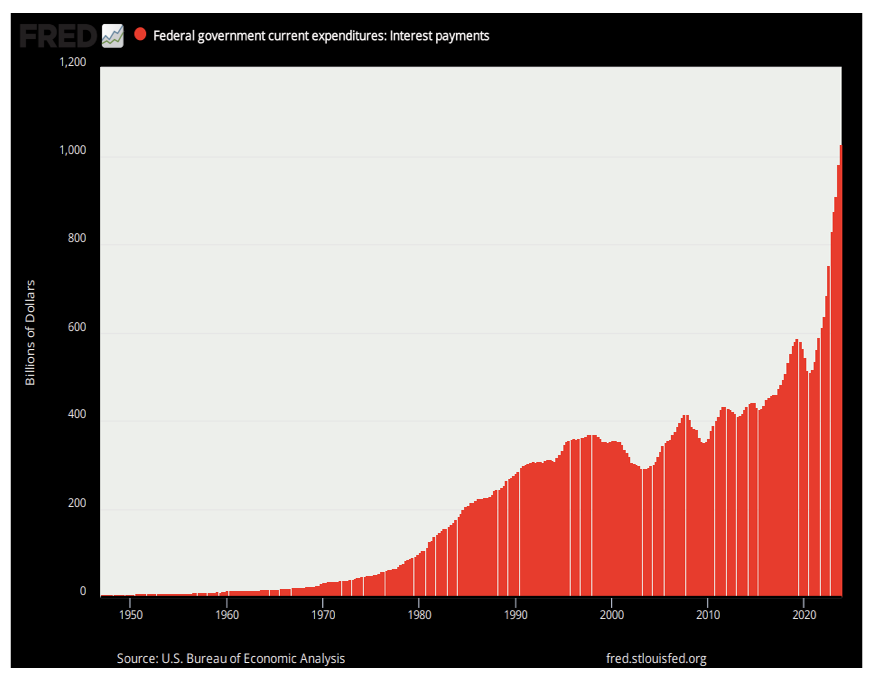

Both the Social Security and Medicare funds covering hospital expenses will begin running red ink in 2035 and 2036, according to fund trustees.

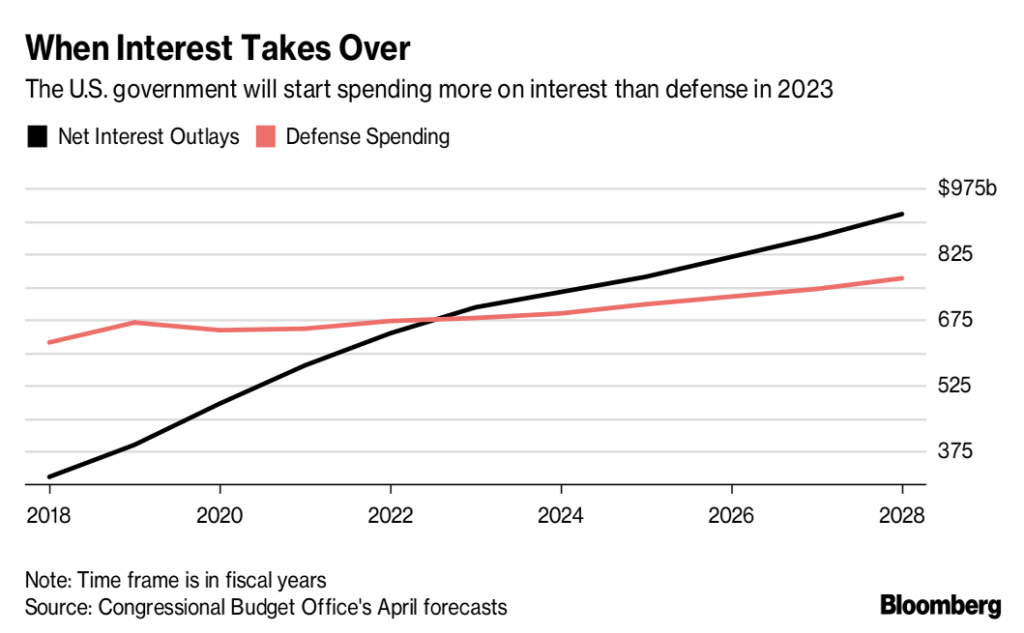

Dr. Paul says that even though interest on the debt is now the third largest item in the federal budget, behind Social Security and Medicare and ahead of military spending, few in Congress are serious about cutting welfare or warfare. They believe the Fed will cover things over by printing money.

The Federal Reserve’s purchase of federal debt will result in price inflation, says Paul.

It will also encourage more government spending by reinforcing the uniparty delusion that, as former Vice President Dick Cheney said, “deficits don’t matter.” The Federal Reserve’s inflationary policies artificially lower the interest rates, which are the price of money. The artificially low interest rates distort the signals sent to investors and entrepreneurs, leading to malinvestment. This creates bubbles resulting in illusionary prosperity. Eventually, economic reality will catch up with the Fed-created illusions and the bubbles will burst, causing an economic downturn.

The next economic crisis will likely either be caused by or result in a rejection of the dollar’s world reserve currency status. Congress will be forced to make drastic cuts in spending while the Fed will be enabled to monetize the debt. This will result in massive public unrest potentially resulting in violence, the rise of authoritarian movements on the left and right, and increasing authoritarianism.

-Ron Paul

During his long tenure in office, Ron Paul was the foremost monetary and gold authority on Capitol Hill. “Those who truly want a monetary system free from political interference should join the movement to restore government’s constitutional limits and separate money and state.”

Until the Constitution is back on top, own gold and silver!

U.S Representative Re-Introduces a Bill that Could Remove Taxes from Coins and Bullion

It is the most audacious flim-flam, for the government to make the nation’s legal tender so unreliable that people have to protect themselves from its devaluation, and then tax them punitively for successfully protecting themselves from it. It’s like installing a clock on your front door, and then the government taxing you on valuables that aren’t stolen.

They intend to get you one way or the other. But maybe they can be stopped!

U.S. Representative Alex Mooney (R-WV) is trying. He has re-introduced The Monetary Metals Tax Neutrality Act (H.R. 8279).

Representative Mooney’s bill would remove all federal income taxation from gold and silver coins and bullion.

U.S. Representative (R) Alex Mooney

“My view, which is backed up by language in the U.S. Constitution, is that gold and silver coins are money and are legal tender,” Rep. Mooney said. “If they’re indeed U.S. money, it seems there should be no taxes on them at all. So, why are we taxing these coins as collectibles?”

Of course, the Deep State Money Manipulators know the monetary performance of gold and silver is far superior to the made-up, unbacked, digitally-printed US dollar. Legal tender laws are intended to force people to use fiat dollars instead of gold and silver, reminiscent of the way Kublai Khan forced his subjects in China to use mulberry bark with his imprint, while he requisitioned all the real money, gold, for himself.

No one ever has to pass a legal tender law to force people to choose superior money that retains its value. They only pass legal tender laws to force people to use money of sketchy provenance and value.

The IRS also classifies gold and silver in the same category as artwork, baseball cards, and other so-called “collectibles.” This applies a higher rate of capital gains taxation than other investments. It’s just another front in the war on gold.

Under Rep. Mooney’s bill, the Monetary Metals Tax Neutrality Act, precious metals gains and losses would not be included in any calculations of a taxpayer’s federal taxable income. It states that “no gain or loss shall be recognized on the sale or exchange of (1) gold, silver, platinum, or palladium minted and issued by the Secretary at any time or (2), refined gold or silver bullion, coins, bars, rounds, or ingots which are valued primarily based on their metal content and not their form.”

Read the bill HERE. Contact Congressman Mooney HERE.

Something is beginning to bubble in the silver market!

The year isn’t even half over and silver is already up more than 15 percent. And yet it is still unbelievably inexpensive!

But first, there is more going on in the silver market than just the insanity of Bidenomics. More than Washington’s unpayable $34.6 trillion national debt. There’s more than just the global dollar standard beginning to fray.

There’s all of that. It’s all rocket fuel for the next big silver move. But there are also the supply/demand fundamentals for silver. They are equally explosive!

The totals from 2023 are in. Industrial demand for silver is setting records. Here are a couple of numbers that grabbed our attention.

Industrial demand for silver rose 11 percent in 2023 to a new record high. At the same time, overall silver supplies are down, including the biggest supply component, mine production.

You might easily have predicted that silver for photovoltaic applications (solar cells) would be higher. But would you have guessed that photovoltaic demand would jump an incredible 64 percent? In just one year?

China figures heavily in the PV sector, and indeed total industrial silver demand from China climber 44 percent in 2023.

Earlier this year we cited one analyst who described silver as “stupidly cheap!” The rising silver price confirms that he’s right.

Silver is still way below its all-time highs. Silver was $50 an ounce in 1980. That was 44 years ago. Are there any other major industrial commodities that are 40 percent below their price of 44 years ago? Don’t kid yourself!

Silver reached highs of about $50 in both 2011 and 2012.

Our point is that silver today is more than 40 percent below its old highs last set a dozen years ago. And there is one thing you need to know about the silver market. When it takes off, it really takes off and even outperforms gold itself!

So now the Federal Reserve has had to backpedal on its presumed interest rate cut this year. That’s due to “a lack of further progress” on inflation says the new policy announcement.

The Deep State Money Manipulators are in one hell of a fix! Again.

If they cut rates and loosen money, prices will keep climbing. If they don’t cut rates, the economy could begin to stall as the decline in GDP suggests.

Wall Street knows that the stock market is driven by the creation of money and credit by the Fed, so the players are obsessed with the game of tea-leaf reading and “dot plots” that are supposed to be indications of what the Fed will do with rates at its next meeting and the one after that and the one after that… They are so good for nothing, they make us laugh!

As recently as March the conventional wisdom was that the Fed would treat Wall Street to three interest rate cuts this year. But what can it do when inflation is in rebound mode and the rest of the world, especially China, wants gold?

So here’s how the Fed hopes to walk the knife edge without falling off. On the one hand, it intends to forego the rate cuts it has been dangling in front of the markets. But on the other hand, beginning in June the Fed is actually going to ease back on “Quantitative Tightening,” its attempt to roll back some of the most frenzied money printing in US history. From the Fed statement:

Beginning in June, the Committee will slow the pace of decline of its securities holdings by reducing the monthly redemption cap on Treasury securities from $60 billion to $25 billion.

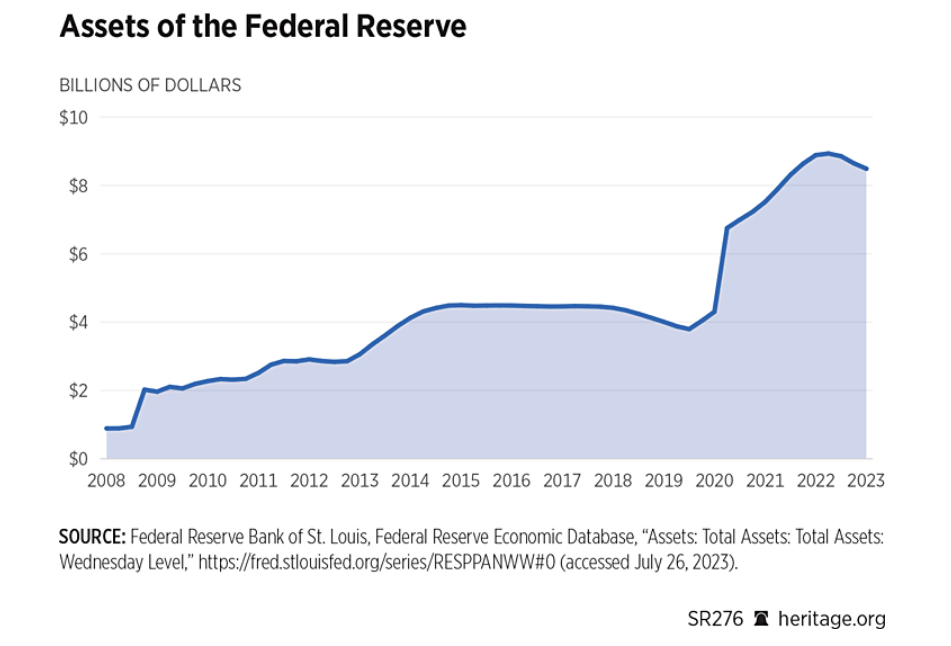

For perspective, from 2008 to this time in 2022, the Fed’s assets – basically the money it “printed” digitally, the money it made up to buy things – ballooned by $8 trillion. Realizing that all that money printing would create new world indoor record inflation, the Fed has been trying to undo some of it while it still can. They set out a long-term schedule for tightening, but now have announced they intend to back off. This means they want to loosen money and credit, but they are afraid that doing so with interest rates will be all too transparent, spurring faster price increases. So, they’re going for the sleight-of-hand rate cut.

At the same time, Chairman Powell sent a clear signal the Fed intends to keep a close watch on the employment numbers. “The employment goal now comes back into focus. So we are focusing on it,” said Powell. That’s Fedspeak for “don’t forget this is an election year!” A weak labor market would be very bad for President Biden and you know our assumption: the Fed will heavily tilt policy to help Biden win reelection.

Monetary policy resembles an old-fashioned pinball machine as it bounces from bumper to bumper. The Fed bounces from inflation to employment, from easing to tightening. All along the way it essentially admits that it doesn’t know what it is doing.

There is no way out. High rates are taking their toll. The cost of funding US debt is soaring. US manufacturing is in contraction, as is employment. But prices keep climbing. Crude oil is up by double-digits since the first of the year. Gas is up more than 20 percent.

“There is a lack of further progress” on inflation. That’s not us. That’s the Fed’s official statement.

Now, doesn’t owning gold make all the sense in the world?

Gross Domestic Product is weak. Inflation is strong. That’s the latest from the government numbers. But all those numbers are misleading. They can be crunched, re-crunched, and inevitably revised. The statistical components are changed at the drop of a hat to serve political interests. And their assumptions are, well, bizarre to say the least. Government spending is a component of GDP. If the government deploys armies of bureaucrats that make the nation less productive, does that make sense as an addition to productivity?

But there is one number that is more or less reliable: US government debt. The government can try to downplay it by saying that some – a lot – of promises it made to people to pay them, things like Social Security, are not part of the debt. Okay. We know what government promises are worth. But the basic debt itself, the money it must borrow to keep afloat, is pretty straightforward.

Today the total public debt is $34.6 trillion. That’s over $100,000 per citizen. This week when you drive by the elementary school in your neighborhood during recess look at all the little kids on the playground. Each one of them owes $100,000, their share of Washington’s debt. How are they going to pay their share?

We’re not trying to make you laugh! But, as Bill Bonner writes, it “makes the $95 billion in ‘foreign aid’ — to people who don’t need it (Israel)… can’t achieve anything with it (Ukraine)… or have no real use for it (Taiwan) — even more out-of-line.

You might like to see the Congressional Budget Office’s projection of the growth of federal debt on the chart from Visual Capitalist below.

Read it and weep! But don’t forget that you can protect yourself with gold and silver. Do you have all you need to get through the coming debt debacle?

A Former Treasury Official Says You Already Don’t!

In YOU WILL OWN NOTHING, Part I, we shared a video of a Canadian man trying to withdraw a few thousand dollars from his bank account. The bank wanted a document of some sort to show what he was going to do with his money.

There is more of this sort of thing going around than most people suspect. It is not just happening at the level of local banks. A former US Treasury official suggests that you may have already lost ownership of your retirement and investment accounts on a national level. You will own nothing!

Meanwhile, the US government is making clear to the rest of the world that their dollar holdings are only theirs when Washington says they can have them.

Locally. Nationally. Internationally. Title to assets and control of monetary resources is under assault. You don’t have to be Carnac the Magnificent to see where this is headed.

On the international front, Congress didn’t just pass a bill to give away $95 billion in foreign aid money we don’t have, it also included a provision that will allow Washington to steal billions of dollars owned by Russia. Bill Bonner says that the measure is the equivalent of if France, in response to the US invasion of Iraq (remember the Weapons of Mass Destruction that didn’t exist?) had seized the bank accounts of Americans in Paris.

This is what is meant by the weaponization of the US dollar. It is why US dollar owners around the world are growing wary of the dollar. They fear correctly that they will own nothing!

That fear is driving a move to more trustworthy alternatives. It explains the move by foreign central banks to own more gold. Gold is the most trustworthy money in the world. It depends on no one’s promise. Gold is its promise!

The US is undermining its own currency. Washington is shooting itself and you in the foot. That is because the value of the dollar has long been buttressed by its international reserve status. Pull out the support system, and everything will cost you even more.

Paul Craig Roberts

What about your ownership of your investment and retirement accounts? Paul Craig Roberts says, “you may have already lost ownership of your banking, pension, and investment accounts.”

Roberts was an assistant secretary of the US Treasury in the Reagan administration and an associate editor of the Wall Street Journal. He explains:

Your “ownership” has been reduced to permission to use your assets until the financial intermediary holding them gets into financial trouble. At that moment, they cease to be your property and become the property of the creditors of the intermediary that holds your accounts, whether it be Merrill Lynch, Schwab, Wells Fargo, TIAA, or whoever. Your dispossession was done quietly over many years by regulatory agencies. This is what Klaus Schwab of the World Economic Forum means when he tells you that “you will own nothing.” You already don’t.

So, there you have it. Faith is collapsing in the property rights the people must have in their financial assets. Internationally. Nationally. Locally. You’ll own nothing… unless you own gold.

The only money you own is gold and silver in your personal possession!

You better watch this video. Especially if you think you own what is in your bank account.

Ownership is the ability to call upon and dispose of assets as you desire or as agreed upon. When you deposit your money into your bank account do you think you still own it?

Better watch this video from Canada…

Apparently you can’t even withdraw your own money from a bank in Canada without being thoroughly interrogated. How is it any of their business what you do with your money? pic.twitter.com/qU0Ktubq9k

During the collapse of major banks last year – Silicon Valley Bank, Signature Bank, First Republic Bank, and others – clients reported personally intrusive inquiries and difficulties in making bank withdrawals. It is a problem that we expect will only grow worse.

Gold is the most liquid financial asset in the world. It is not dependent on counterparties, fund managers, bank managers, or Fed officials. It is not susceptible to being frozen by bank holidays or by institutional bankruptcies.

But this only applies to physical gold and silver you have in your possession. It does not apply to “paper gold” or gold substitutes. To learn more about the safety of gold, speak with a Republic Monetary Exchange precious metals professional today!

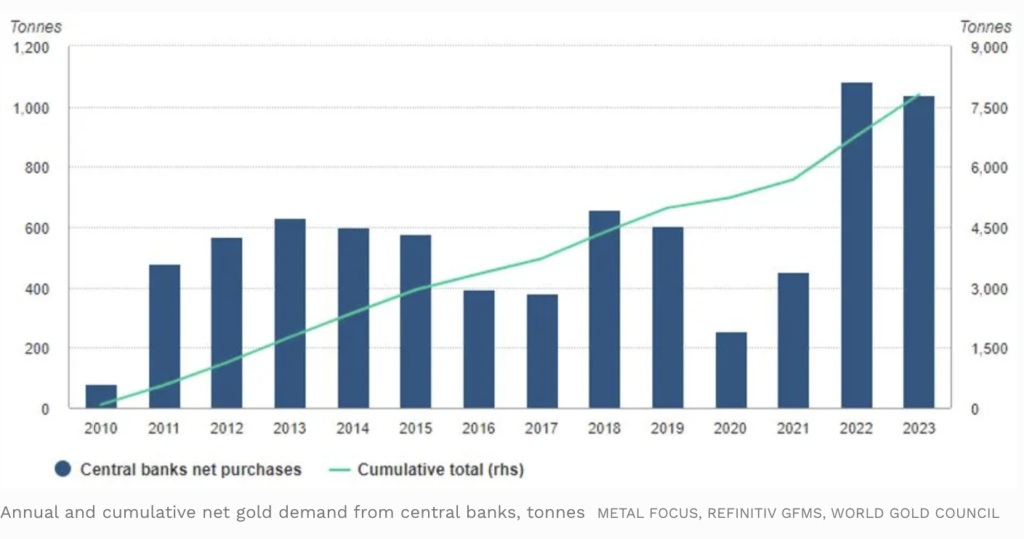

Why are global central banks beating a pathway to the gold market? Why are central banks an important force in driving the gold price to new all-time highs?

We have called central bank de-dollarization and gold-buying one of the most important megatrends of our time. Now a new World Bank publication spells out why this is happening, and it does so in a candid way that makes a powerful case for individuals to protect their wealth with gold.

In recent years, gold has regained its importance as a financial asset, with many investors using it as a hedge against inflation and market volatility. In addition, central banks and other financial institutions continue to hold significant amounts of gold as part of their reserve assets.

The role of gold as a reserve asset for central banks has been a significant driver of demand for the precious metal. Gold is also considered a safe haven asset during times of economic uncertainty and geopolitical turmoil, making it a popular among investors looking to hedge against market volatility.

Here are a couple of bullet points from the new World Bank handbooks…

Geopolitical risk is a major factor for asset managers to consider, especially in emerging markets. This is because geopolitical events can have significant impact on financial markets, as seen in the freezing of the assets of the Iranian Central Bank ($1.9 billion) in 2010, the Kazakhstan National Bank ($22.6 billion) in 2017, the Venezuelan Central Bank ($342 million) in 2020, the Afghan Central Bank ($7 billion) in 2021, and most recently the Russian Central Bank (estimated at $258 billion).

The belief is that the Russian sanctions create incentives for central banks to abandon the dollar in favor of gold and for governments to cash in their dollar reserves for stocks of other commodities. Overall, the recent sanctions against Russia highlight the importance of gold as a reserve asset.

Gold’s liquidity surpasses the major financial assets and government debt markets of many developed economies.

Gold has proven to be a reliable and stable investment over the medium and long term. Since the fall of the “gold standard” in 1971, gold has delivered an average annual return of around 11 percent, with a compounded annual growth rate (CAGR) of 8 percent.

Gold offers positive real returns during periods of low, moderate, and high inflation (Figure17). Notably, aggregate US Treasuries produced positive real returns only during periods of low inflation, whereas broad US equities, while offering high returns during periods of low and moderate inflation, typically suffer from large losses when inflation exceeds 3 percent on a consistent basis.

For protection from geopolitical risk, from government policies that prevent you from the use of your own money, for liquidity, stability, and superior returns, speak to a Republic Monetary Exchange precious metals expert about adding gold to your portfolio.

Gold is going through the roof because the already unpayable US debt is, too!

After all, if there is no hope for US debt at $34 trillion today, how about when it reaches $141 trillion in 2054? And that is where the Congressional Budget Office says we are headed!

$141 trillion is a lot of money! How does a national government even begin to pay the interest on a debt that big? You know the answer: money printing!

Former Federal Reserve Chairman Ben Bernanke was both candid and shameless about it just a few years ago: “The US government has a technology, called a printing press, that allows it to produce as many dollars as it wishes at essentially no cost.”

Look, from 2024 to 2054 the annual deficits will average 6.7 percent of GDP. That is almost double their average over the last half-century!

By 2054 the deficit will hit 8.5 percent of GDP.

Says the CBO, apparent master of understatement, “Such large and growing debt would have significant economic and financial consequences.”

Among its other effects, it would slow economic growth, drive up interest payments to foreign holders of U.S. debt, heighten the risk of a fiscal crisis, increase the likelihood of other adverse outcomes, and make the nation’s fiscal position more vulnerable to an increase in interest rates.

When we want to print something, we have to buy inkjets, make sure there is plenty of paper in the printer and hit Control P. Today the Fed’s legalized money printing is mostly digital. It’s so easy now! They don’t even have to cut down all those trees for paper like they used to do! They must be environmentally friendly!

Make sure you have plenty of US gold coins, Maple Leafs, Krugerrands, other favorite coins, and gold bars! And don’t forget the silver – bars and coins! You’ll need it!

Here’s a story we have told before, but with gold hitting so many all-time highs lately, it is one that deserves to be told again.

It begins with a serious economic crisis that is fast approaching. Here’s a snippet from Fred Hickey (The High Tech Strategist) on April 2 that highlights just how fast things are spinning out of control. In just the last 20 days, he writes, US government debt increased by $168 billion. That is equal to the entire US deficit in 2002!

This unrelenting gusher of red ink ensures that something like a “Crack-Up Boom” is fast approaching today.

That is the name the great free-market economist Ludwig von Mises coined to describe the last stage of a currency breakdown: The Crack-Up Boom. In German, it is “Katastrophenhausse,” a catastrophe boom.

Because we think our friends and clients will need to know very soon, from his work Human Action, here is Mises’ description of the breakdown of a currency:

The characteristic mark of this phenomenon is that the increase in the quantity of money causes a fall in the demand for money…. The monetary system breaks down; all transactions in the money concerned cease; a panic makes its purchasing power vanish altogether. People return either to barter or to the use of another kind of money.

The course of a progressing inflation is this: At the beginning the inflow of additional money makes the prices of some commodities and services rise; other prices rise later. The price rise affects the various commodities and services, as has been shown, at different dates and to a different extent.

This first stage of the inflationary process may last for many years. While it lasts, the prices of many goods and services are not yet adjusted to the altered money relation. There are still people in the country who have not yet become aware of the fact that they are confronted with a price revolution which will finally result in a considerable rise of all prices, although the extent of this rise will not be the same in the various commodities and services. These people still believe that prices one day will drop. Waiting for this day, they restrict their purchases and concomitantly increase their cash holdings. As long as such ideas are still held by public opinion, it is not yet too late for the government to abandon its inflationary policy.

But then finally the masses wake up. They become suddenly aware of the fact that inflation is a deliberate policy and will go on endlessly. A breakdown occurs. The crack-up boom appears. Everybody is anxious to swap his money against “real” goods, no matter whether he needs them or not, no matter how much money he has to pay for them. Within a very short time, within a few weeks or even days, the things which were used as money are no longer used as media of exchange. They become scrap paper. Nobody wants to give away anything against them.

It was this that happened with the Continental currency in America in 1781, with the French mandats territoriaux in 1796, and with the German Mark in 1923. It will happen again whenever the same conditions appear. If a thing has to be used as a medium of exchange, public opinion must not believe that the quantity of this thing will increase beyond all bounds. Inflation is a policy that cannot last.

“Inflation is a policy that cannot last.”

That is why gold has broken out for new higher ground at the same time Federal Reserve Chairman Jerome Powell has admitted once again that the Fed doesn’t really know what it is doing.

China, once America’s leading creditor, is fleeing US government bonds like they have the plague. It is doing so at the same time that the governments need to borrow more money than ever.

The Crack-Up Boom is nearing. Do you have all the gold and silver you need?

It’s a gold and silver bull market for all the reasons we’ve been saying. As we write this, spot gold is about $2,400, while Spot silver is closing in on $29.00 per ounce.

Why are precious metals so strong, especially in a rising interest rate environment?

Because other countries are fed up with dollar inflation. US debt has gone stratospheric, and the swamp creatures don’t care. Their cronies are stealing everything, and Washington wars are making us poorer.

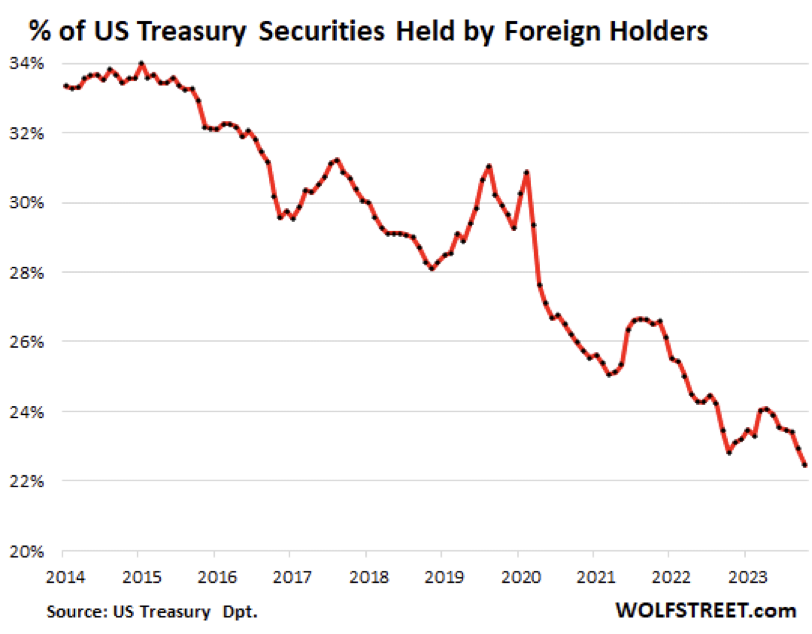

Just a decade ago foreign investors and foreign central banks owned about 43 percent of all outstanding US government debt. That has now fallen to about 30 percent.

Washington has given no sign that it is going to do anything about soaring US debt. On the contrary, its spending continues to grow ever more reckless. Some of that spending is driven by forces out of the hands of Capitol Hill. Rising interest rates are hitting hard. The average interest on US government debt is now 3.2 percent. That may seem low, but it is the highest it has been since 2010 and as old debt at low rates matures, it has to be refinanced at prevailing rates that are much higher.

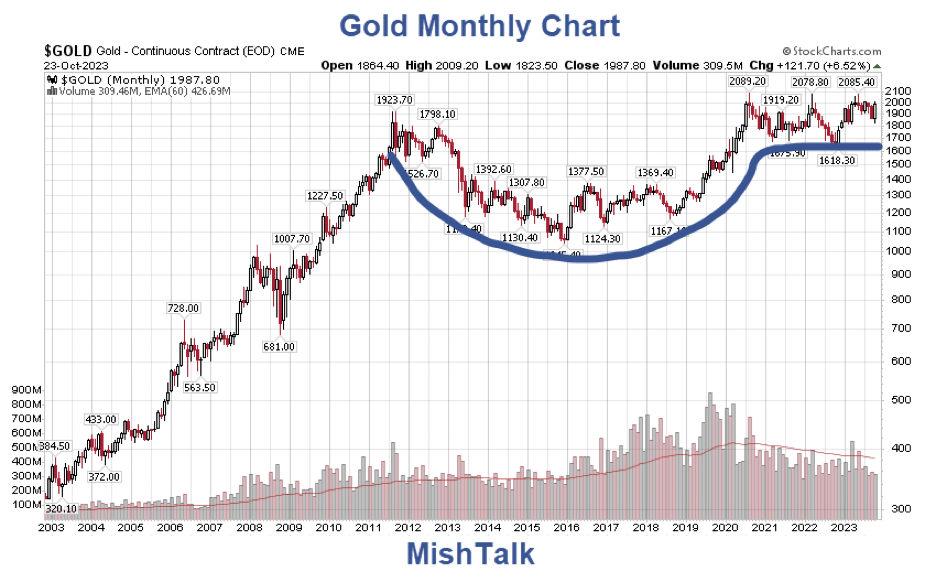

It was in 2020 that gold first traded above $2,000 an ounce.

As you can see, gold topped at just below $2,100 three times, in in August ’20, March ’22, and May ’23. Now after four years of range-bound trading, gold has run through all the overhead resistance like a hot knife through butter.

Spot silver has peaked at about $50 an ounce three times, first back in 1980, and more recently in 2011 and again in 2012.

Don’t miss this bull market. The US dollar is losing its global reserve might, while silver is still way below its all-time highs. And gold has a long way to go!

We believe the price of gold is confirming that Washington’s debt is every bit as bad as we have said.

Our opinions don’t have the force of law, but to us the US national debt is a matter of criminal negligence. Washington has been indifferent to the debt as it grew, and now it is too late: the national debt has gotten away from us!

From the Wall Street Journal:

The Congressional Budget Office reported Monday that the federal budget deficit for the first six months of fiscal 2024, ending in March, was $1.064 trillion. Enjoy it, because you’ll eventually pay for it in higher taxes.